If you have the resources to consider buying property in Nepal outright—congratulations, you are in a fortunate financial position. But “can I pay cash?” and “should I pay cash?” are very different questions. In Nepal’s current market environment, the decision between taking a home loan and paying cash is genuinely nuanced, with meaningful financial arguments on both sides. Here is a thorough analysis to help you decide.

Overview

At first glance, paying cash seems obviously superior—no interest costs, no monthly EMI obligations, immediate full ownership. But cash used to buy property is cash that cannot be deployed elsewhere. And with Nepal’s home loan interest rates at 9–12% per annum, the “cost” of borrowing must be weighed against the “opportunity cost” of tying up significant capital in an illiquid asset. The right answer depends on your specific circumstances, investment alternatives, and risk tolerance.

The True Cost of a Home Loan in Nepal

Let us run the numbers on a NPR 1 crore home loan at 10% per annum over 20 years:

- Monthly EMI: approximately NPR 96,500

- Total repayment over 20 years: approximately NPR 2.32 crore

- Total interest paid: approximately NPR 1.32 crore

This means a NPR 1 crore loan costs NPR 2.32 crore in total—a very significant premium. However, this must be compared against what your NPR 1 crore could earn if invested elsewhere over the same 20 years.

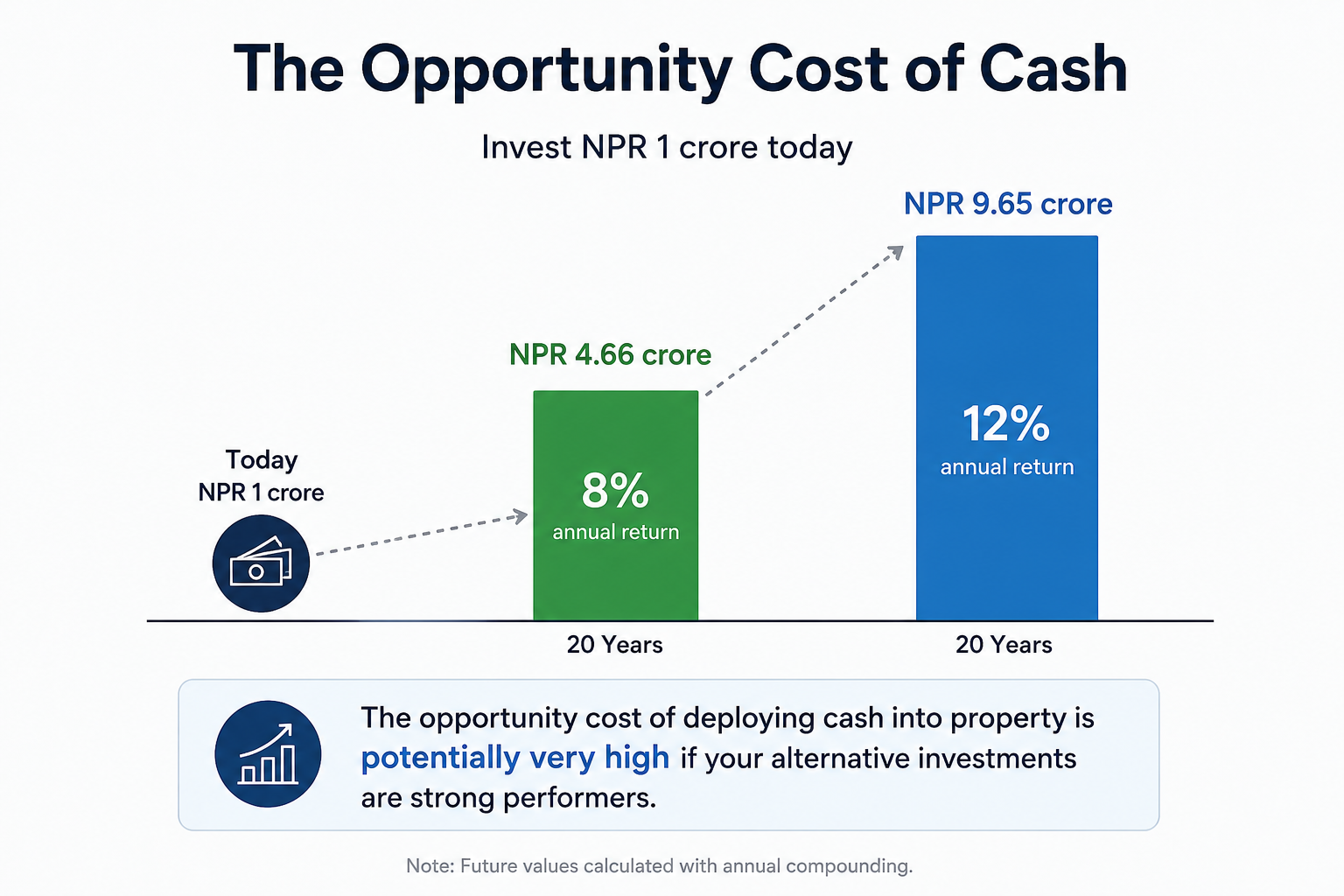

The Opportunity Cost of Cash

If you invest NPR 1 crore in a diversified portfolio earning a conservative 8% annual return over 20 years, you would accumulate approximately NPR 4.66 crore. At a more optimistic 12% return (achievable through equity markets or strong commercial property yields), the same NPR 1 crore grows to approximately NPR 9.65 crore. The opportunity cost of deploying cash into property is therefore potentially very high if your alternative investments are strong performers.

Break-Even Analysis

The break-even question is: at what rate of property appreciation does owning outright (vs. taking a loan and investing the cash) produce the same wealth outcome? At Nepal’s current home loan rates (10%) and conservative investment returns (8%), the break-even property appreciation rate is approximately 5–6% per annum. Properties in good Kathmandu locations have historically appreciated at 8–12%—suggesting that owning outright is not necessarily superior to leveraging via a loan and investing the freed capital.

Tax Implications

Nepal currently offers limited tax deductions on home loan interest for individual taxpayers compared to some international markets. Consult a tax advisor on the current position, as tax treatment is subject to change in annual budgets.

When Cash Purchase Wins

- You are purchasing at retirement age and want zero monthly financial obligations

- Your alternative investment options are limited or risky

- You are purchasing a property where the rental yield covers or exceeds the opportunity cost of capital

- You are risk-averse and the psychological value of debt-free ownership is significant to you

- You can negotiate a meaningful price discount for a quick, clean cash transaction (5–10% discounts are achievable)

When a Home Loan Wins

- You have better-yielding investment alternatives for the capital

- You are earlier in your career and building wealth through multiple channels

- Leveraging a loan allows you to purchase a higher-quality property than cash alone permits

- Property appreciation is expected to comfortably exceed the loan interest rate

Need help modelling your specific scenario? Speak to a Basobaas financial advisor—we help buyers navigate the financing decision for free.

")