")

For most Nepali families, a home loan is the bridge between dreaming of owning property and actually making it happen. Nepal’s banking sector offers a range of home loan products, but navigating interest rates, eligibility criteria, documentation requirements, and the application process can be overwhelming—especially for first-time buyers. This guide, written from experience with Nepal’s real estate market, gives you everything you need to secure the right home loan in 2026.

Home Loan Overview in Nepal

Home loans in Nepal are offered by commercial banks, development banks, and finance companies, all regulated by Nepal Rastra Bank (NRB). NRB guidelines set the framework for loan-to-value (LTV) ratios, interest rate bases, and lending limits. As of 2026, banks can lend up to 60–70% of the government-assessed property value for residential home loans, meaning buyers typically need a 30–40% down payment.

Top Banks Offering Home Loans in Nepal

Most major commercial banks in Nepal offer competitive home loan products. These include Nepal Bank Limited, Rastriya Banijya Bank, NMB Bank, Global IME Bank, Nabil Bank, Standard Chartered Bank Nepal, Himalayan Bank, and Kumari Bank, among others. It is worth obtaining quotes from at least 3–4 banks, as rates and terms vary significantly. Development banks and microfinance institutions may also offer products for buyers in rural areas or smaller loan amounts.

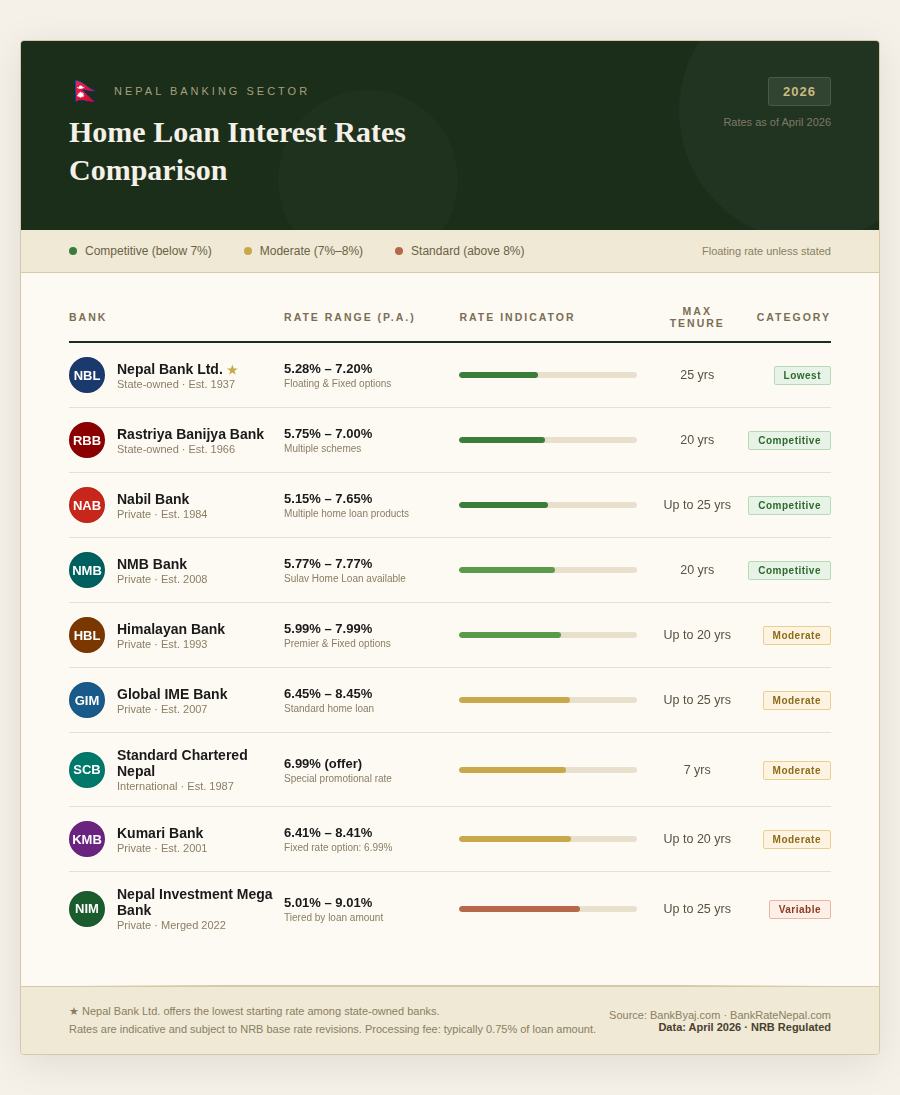

2026 Home Loan Interest Rates

Home loan interest rates in Nepal fluctuate based on the base rate set by individual banks (itself influenced by NRB policy) plus a premium. As of early 2026, typical home loan interest rates range from approximately 9% to 12% per annum, with some banks offering slightly lower introductory rates for the first 1–2 years. Fixed-rate and floating-rate options are both available. Floating rates carry the risk of rising if the base rate increases, while fixed rates provide certainty but are usually set higher.

Eligibility Criteria

While each bank has slightly different criteria, the general eligibility requirements for a home loan in Nepal include:

- Nepali citizenship (NRN citizens with NRN card may have additional provisions)

- Age: typically 21–65 years at the time of application (loan must be repaid before age 65–70)

- Stable income: salaried employees, business owners, and professionals. Banks typically require a minimum monthly income that is 2–3x the proposed EMI

- Credit history: banks will check your credit record with the Credit Information Centre (CIC)

- The property being purchased must be in Nepal and acceptable to the bank as collateral

Required Documents

- Citizenship certificate (original and photocopy)

- Recent passport-size photographs

- Income proof: salary slips (last 3–6 months), bank statements (last 6–12 months), and/or IT returns

- Property documents: Lalpurja, land parcel map, tax clearance

- Property valuation report (commissioned by the bank)

- PAN card

- For business owners: business registration, VAT/PAN registration, audited financials

The Application Process

- Get a preliminary eligibility assessment from your chosen bank (most offer this free)

- Identify your property and have the bank conduct a formal valuation

- Submit the complete loan application with all required documents

- Bank conducts credit assessment and approves the loan amount

- Sign the loan agreement and mortgage deed

- Funds are disbursed—often directly to the seller or in stages for under-construction properties

Tips to Get Approved

- Clear any existing loans or credit card dues before applying—your debt-to-income ratio matters

- Maintain a clean bank account history with regular salary credits for at least 6 months before applying

- Avoid multiple simultaneous loan applications—each one creates an inquiry on your credit record

- Choose a property with clean documentation—banks will reject applications where property title is unclear

Need help connecting with home loan advisors? Contact the Basobaas team—we partner with Nepal’s leading banks to help buyers find the best home loan deals.

")